The financial media is salivating over the whisper of a $135 SpaceX initial public offering. Wall Street analysts are already churning out valuation models, calculating price-to-earnings multiples, and drafting gushing notes about retail investors finally getting a piece of the launch monopoly.

They are fundamentally misreading the entire board.

An IPO for SpaceX is not the triumphant next step of commercial spaceflight. It would be a structural execution. The narrative that going public democratizes access to space technology is a fantasy sold by investment bankers looking for a payday. If you understand corporate governance, capital structures, and the raw physics of interplanetary exploration, you know that a public SpaceX would immediately collapse under the weight of quarterly earnings expectations.

Buying into a SpaceX IPO at $135 isn't investing in the future. It is funding the bureaucratic strangulation of the most aggressive engineering firm on the planet.

The Quarterly Earnings Death Trap

Public markets demand predictability. They want smooth, upward-sloping charts, predictable margins, and reliable share buybacks.

SpaceX operates on a model of calculated, spectacular failure.

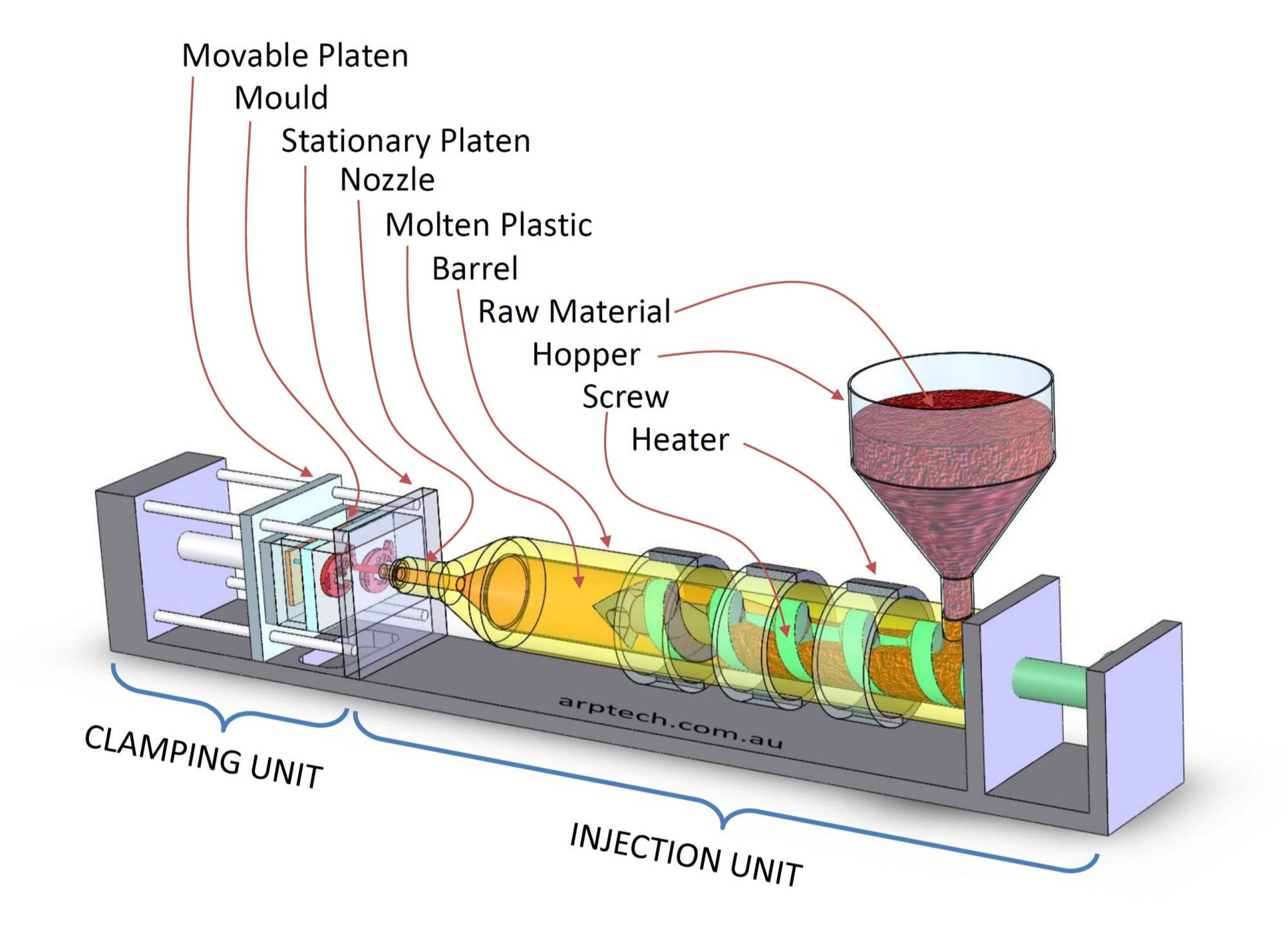

When a Starship prototype explodes over the Gulf of Mexico during a developmental test flight, private engineers celebrate the telemetry data gained. The private structure allows the company to absorb a half-billion-dollar hardware loss in an afternoon without answering to a single panicked fund manager.

Imagine that same explosion occurring while answering to public shareholders.

The stock would plummet 20% in after-hours trading. Risk-averse institutional boards would demand independent committee investigations. Activist investors would buy up blocks of shares, secure board seats, and immediately demand the cancellation of the unproven Starship program to protect the highly profitable, recurring revenue of the Falcon 9 and Starlink divisions.

Private Governance: Test -> Explode -> Learn -> Rebuild in 3 Weeks

Public Governance: Test -> Explode -> SEC Investigation -> 6-Month Delay -> Stock Crash

I have watched public tech legacy giants torch their R&D budgets the second a bad quarter hit because the executive team needed to pump the stock price before their options expired. Public incentives favor preservation over innovation. The moment SpaceX accepts public money, the mission shifts from colonizing Mars to hitting Q3 consensus estimates.

The Physics of Capital: Why SpaceX Does Not Need Your Cash

The core premise of an IPO is capital formation. Companies go public because they have exhausted private funding or need a massive war chest to scale operations.

SpaceX is currently printing cash.

The Starlink satellite constellation has crossed the cash-flow positive threshold. It operates as a global internet utility with a captive market, funding the capital expenditure of the Mars program internally. According to launch manifests and defense contract data, the company maintains a near-total monopoly on commercial and national security launches.

Furthermore, the private market appetite for SpaceX equity is insatiable. Whenever the company needs liquidity for employee stock options or specific projects, it orchestrates secondary tender offers. Private private equity funds, sovereign wealth funds, and ultra-high-net-worth individuals fight for allocations.

Why would executive leadership trade sovereign control for public money when they can raise billions on a weekend via private placements without disclosing proprietary engineering metrics to competitors? They wouldn't. The rumor of a $135 IPO is a valuation anchor used for private funding rounds, not a roadmap to the New York Stock Exchange.

Demolishing the Starlink Spin-off Myth

A common counter-argument from retail bulls is that SpaceX will spin off Starlink as a separate public entity, leaving the deep-space exploration private.

This view ignores the physical and financial architecture of the enterprise.

Starlink and Starship are not separate businesses; they are two organs in the same body. Starlink requires the massive payload capacity and low cost-per-kilogram of Starship to deploy its next-generation, heavier V3 satellites at scale. Conversely, Starship requires the massive, high-margin revenue generated by Starlink's global consumer and military subscriptions to fund its development.

Separating them via a public spin-off creates an immediate conflict of interest. A public Starlink board would be legally obligated to seek the cheapest launch provider to maximize shareholder value. If a competitor somehow underbid Starship, or if Starship development lagged, the public entity would face lawsuits for favoring its private parent company.

The operational dependencies are too tightly wound. You cannot slice the cash cow away from the rocket factory without bleeding both entities dry.

The Brutal Reality for Retail Investors

Let’s look at the math of a hypothetical $135 listing price. At that level, the implied valuation sits north of $200 billion.

If you buy in at the IPO, you are not getting in early. You are buying at the absolute top of the private valuation curve. The venture capitalists, early employees, and institutional insiders who bought in when the company was valued at $10 billion are looking for an exit. A public offering at $135 is an invitation for retail investors to act as liquidity providers for the smart money.

The Real Risks Nobody Lists in the Prospectus:

- Regulatory Weaponization: A public SpaceX becomes a massive target for regulatory agencies, environmental lawsuits, and unionization efforts that can cripple operational speed.

- Key Man Dependency: The valuation is inextricably tied to volatile leadership. A single corporate scandal or sudden departure would wipe out tens of billions in market cap instantly.

- Geopolitical Vulnerability: Starlink is active in active conflict zones. A public company faces severe shareholder liability and international compliance sanctions that private entities can navigate with far greater agility.

Stop Asking When You Can Buy SpaceX Stock

The question "When is the SpaceX IPO?" reveals a fundamental misunderstanding of wealth creation in the modern era. The most disruptive companies no longer need the public markets to scale. They stay private longer, capture 99% of the growth within closed networks, and only go public when growth slows and the insiders want to cash out.

If you want a stable, dividend-paying aerospace utility that moves at the speed of a government contract, buy Boeing or Lockheed Martin. Watch them spend more time navigating compliance and satisfying activist shareholders than building functional hardware.

SpaceX works precisely because it treats the public market with complete indifference. The day a ticker symbol appears next to its name is the day the mission to Mars officially dies. Stay away from the hype, ignore the $135 anchor price, and realize that some of the greatest engines of human progress are designed to exist completely outside the casino of Wall Street.